Estate Tax Updates for 2023

Happy New Year! With each new year comes adjustments to the existing estate tax exemptions that all practitioners and clients alike should be aware of. As inflation skyrocketed during 2022, ...

Happy New Year! With each new year comes adjustments to the existing estate tax exemptions that all practitioners and clients alike should be aware of. As inflation skyrocketed during 2022, ...

Weather motivates some; politics motivates others; the ability now to work remotely and spend less on housing costs is also often cited as a reason for wanting to leave… and… ...

Charitable planning is gaining popularity not just for those with philanthropic desires, but also for those looking to take advantage of certain tax benefits that charitable planning may provide. The ...

On June 21, 2019, the U.S. Supreme Court unanimously decided North Carolina Department of Revenue v. Kimberley Rice Kaestner 1992 Family Trust, holding that The Due Process Clause does not permit ...

On May 29, 2019, the New York State Department of Taxation and Finance released Technical Memorandum TSB-M-19(1)S highlighting some of the Sales and Use Tax changes enacted in the 2019-2020 ...

As the April 15th deadline for filing 2018 income tax returns draws near (April 17th for Maine, Massachusetts and the District of Columbia), many taxpayers may face a situation in ...

In one of our previous blog posts, we discussed the growth of trusts that are utilized specifically to be named as beneficiaries of retirement accounts, and the various benefits associated with ...

Sales tax….no one likes collecting it and no one likes paying it. How many times have you heard a business owner say “but if you pay me cash…” How many ...

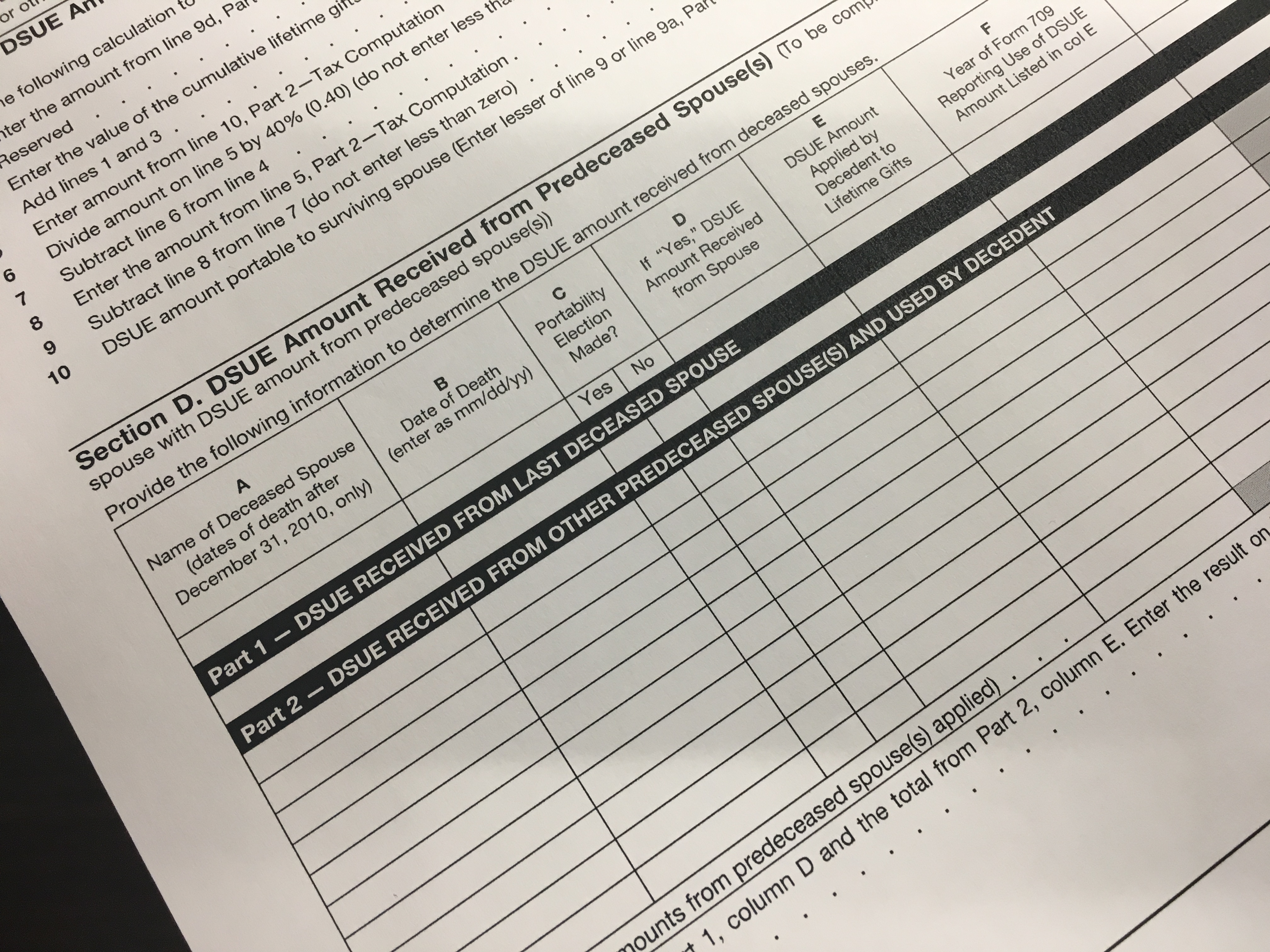

As enacted by the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 and made a permanent part of the Internal Revenue Code by the American Taxpayer Relief ...